Beautiful luxury home for sale in Farragut’s Bridgemore subdivision. Designed by Jack Herr & Associates and built by BrookWood Construction for the 2013 Parade of Homes, this home sets itself apart from most other homes on the market. The open floor plan concept utilizes over 3000SF just on the main level (the total square footage is 4922SF). Kitchen, family room, keeping room, and breakfast room are all adjoined and share views of the Smoky Mountains. The mountains can also be enjoyed from the main level master suite which exits to the outdoor entertaining areas featuring a covered porch with outdoor fireplace and a custom grilling area with bar seating. 3 additional bedrooms upstairs plus home theater room with 3 TV’s and automated blinds. For additional information on Bridgemore Knoxville, 815 Hammock Lane, Knoxville, TN 37934, or to schedule a private showing contact me, Troy Stavros with Gables & Gates, REALTORS.

This listing is no longer available.Jimmy Haslam Puts His Knoxville Luxury Home Up For Sale

Jimmy Haslam and his wife Susan have put their Knoxville luxury home up for sale. Haslam, the CEO of Pilot Flying J and majority owner of the Cleveland Browns purchased this home, located at 5020 Lyons View Pike back in 1996. The historic Tudor home was built by Charles I. Barber in 1928. This incredible lakefront home takes advantage of stunning views of the Smoky Mountains and the Tennessee River. The Haslams did an incredible job of keeping the integrity of the original architecture while undergoing a complete renovation which included additions to the home.

Jimmy Haslam and his wife Susan have put their Knoxville luxury home up for sale. Haslam, the CEO of Pilot Flying J and majority owner of the Cleveland Browns purchased this home, located at 5020 Lyons View Pike back in 1996. The historic Tudor home was built by Charles I. Barber in 1928. This incredible lakefront home takes advantage of stunning views of the Smoky Mountains and the Tennessee River. The Haslams did an incredible job of keeping the integrity of the original architecture while undergoing a complete renovation which included additions to the home.

Per the listing description (see below for pictures):

“5020 Lyons View is bordered with one of a kind dramatic views, exquisite gardens, stone terraces, custom flowing fountain, secluded pool side retreat with charming bath house, screened pavilion and private gathering deck which overlook the skyline view of our Tennessee River and Smoky Mountains. Lyons View allows you to define your extraordinary lifestyle with the wide and varying mix that includes classic details and modern amenities. Please notice the superb and exceptional interior and exterior details as the unsurpassed quality and charm can’t be duplicated. Seamless integration of indoor and outdoor spaces are achieved through free-flowing casual living spaces.

Family gatherings or entertaining guests is a joy in this amazing Epicurean Gourmet Kitchen/Gathering Room. In the heart of the home one will enjoy the large center island / 6 burner gas viking range, stainless venting hood/warming drawers/sub zero refrigerator/abundance of built -in cabinetry/limestone fireplace ….and of course the true Tudor flavor of diamond cut casement windows!!

The Grand Hall has been lovingly crafted with the utmost attention to sophisticated details……Boasting architectural features inspired by travels include handsome slate flooring and english designed “Rumford” fireplace with a vintage handcrafted facade. Dramatic tongue and groove painted ceiling with custom engineered Amdega Atrium Windows graciously bring in the outdoors from above, while a wall of casement windows showcase the breathtaking view of the estate, Tennessee River, Smoky Mountains as well as lush meticulously maintained gardens. Several custom french doors exit to various

verandas and terraced settings with an exceptional outdoor fireplace and custom designed fountain.

Extraordinary Master Suite Retreat is Relaxing and Private with Attractive Appointments!

French doors exit to upper level decking with glorious view of the estate and breathtaking vistas.

Multiple closet options include walk-ins with custom built-ins..

Individual porcelain pedestal sinks add such a timeless classic element

Exquisite marble wall accents, spacious walk-in marble steam shower, large jetted oval soaking tub, custom built-ins, make-up and linen closet are a few more details to

embrace.

Private Pool is completely enclosed with classic wrought iron fencing….as is the entire estate.

Let this Exquisite Home with it’s timeless formal and casual living spaces become part of your family’s lifestyle. Lyons View’s Tudor Gem is a well crafted Knoxville masterpiece and one you will be pleased to own and enjoy!!!”

For information on this home or any other home in the Knoxville or Farragut area, contact me, Troy Stavros with Gables & Gates, REALTORS. I look forward to talking with you!

This listing is no longer available.Buying a Knoxville Home With Only A 3% Down Payment

Did you know that buying a home in Farragut or Knoxville can now be done with only a 3% down payment? In an effort to open up the possibility of home ownership to more Americans, Freddie Mac and Fannie Mae have both launched programs only requiring a 3% down payment. While Fannie Mae’s program is limited to first time home buyers or buyers who haven’t owned a home in the past 3 years, Freddie Mac’s program does NOT have these limitations. Freddie Mac has what they are calling the Home Possible Advantage Mortgage. In their own words it is: “An affordable, conforming, conventional mortgage with a 3% downpayment requirement designed to make responsible homeownership accessible to more first-time buyers and other qualified borrowers with limited downpayment savings.”

Did you know that buying a home in Farragut or Knoxville can now be done with only a 3% down payment? In an effort to open up the possibility of home ownership to more Americans, Freddie Mac and Fannie Mae have both launched programs only requiring a 3% down payment. While Fannie Mae’s program is limited to first time home buyers or buyers who haven’t owned a home in the past 3 years, Freddie Mac’s program does NOT have these limitations. Freddie Mac has what they are calling the Home Possible Advantage Mortgage. In their own words it is: “An affordable, conforming, conventional mortgage with a 3% downpayment requirement designed to make responsible homeownership accessible to more first-time buyers and other qualified borrowers with limited downpayment savings.”

I meet plenty of folks who would love to own their own home, but have not had the ability, because of many different circumstances, to save up 10 or 20% for a down payment. This could be a game changer for them!

According to Dave Lowman, Executive Vice President of Single-Family Business at Freddie Mac: “Home Possible Advantage gives qualified borrowers with limited downpayment savings a responsible path to homeownership and lenders a new tool for reaching eligible working families ready to own a home of their own. Home Possible Advantage is Freddie Mac’s newest effort to foster a strong and stable mortgage market.” Lowman continued: “There’s a new reason Realtors and lenders may expect more qualified borrowers at the closing table during this spring’s home buying season. In addition to low mortgage rates and rising job growth, the down payment hurdle is starting to shrink for creditworthy borrowers, including first-time homebuyers.”

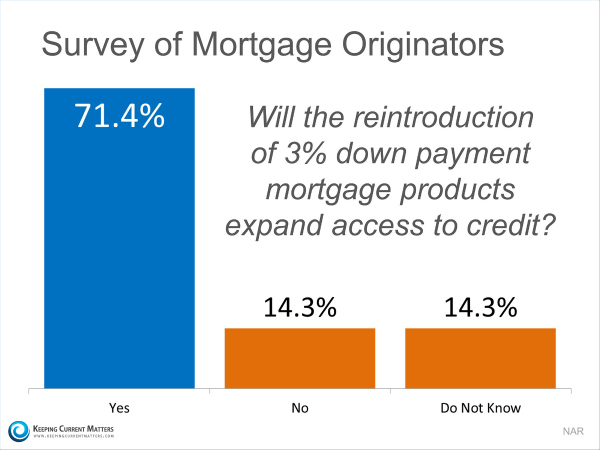

It appears that Lowman is in agreement with the mortgage industry, as a recent survey conducted by the National Association of REALTORS, while polling mortgage professionals, showed that most loan officers feel that the ability to offer a lower downpayment option will increase access to mortgage money. Here is what the survey found:

Here are some key facts about the Home Possible Advantage Program:

- Home Possible Advantage offers qualified low- and moderate-income borrowers a conforming conventional mortgage with a maximum loan-to-value ratio of 97 percent.

- Home Possible Advantage mortgages can be used to buy a single unit property or for a “no cash out” refinance of an existing mortgage.

- First time homebuyers must participate in an acceptable borrower education program, like Freddie Mac’s CreditSmart®, to qualify for Home Possible Advantage.

- Home Possible Advantage mortgages are available as 15-, 20-, and 30-year fixed rate mortgages.

Here are some answers to frequently asked questions:

- Can first-time buyers use the 97% LTV program to purchase a home? Yes. The 97 percent program can be used by first-time buyers. It can also be used by repeat buyers.

- How can I come up with the money for down payment and closing costs? Ways to come up with the down payment are using your own savings or using “gift funds.” Acceptable donors of gift funds are your fiancée, domestic partner, spouse, child or other dependent, or any individual related to you by blood, marriage, adaption or legal guardianship.

- Is the low-downpayment mortgage program via Fannie Mae and Freddie Mac better than a FHA loan? What’s best for one home buyer may not be what’s best for another. Each program has its benefits. I would be happy to introduce you to our preferred lender who can counsel you to find out which program would work best for your situation.

- What is the loan limit on the 3% down program through Fannie Mae and Freddie Mac? The 3% downpayment program is limited to loan sizes of $417,000 or less. Loans in higher-cost areas are permitted, but loan sizes remain capped at local conforming loan limits.

- Can this program be used to refinance my current home? YES. Eligible homeowners who wish to refinance their current mortgage can refinance their loan up to the 97% loan to value level. There are certain limitations so check with our preferred mortgage professional for details.

- Are vacation homes eligible under the 3% downpayment program? No, the 3% downpayment program is for primary residences only. Vacation and second homes are not allowed.

- Can the 3% downpayment program be used for investment properties? No, the 3 percent down-payment program is for primary homes only. Investment properties are not allowed.

- Is private mortgage insurance required with the 97% mortgage program? Yes, mortgage applicants are required to pay private mortgage insurance (PMI) as part of the 97% mortgage program. Your mortgage lender will arrange for your mortgage insurance policy at the time of application.

- Will low down payment loans cause another housing collapse like the sub-prime mortgages did? I say no and here is why. Unlike the problem loans of the past, the level of documentation required to obtain these loans is far more in depth. Prospective buyers will be expected to document all details of their financial situation with everything from income, employment, and financial documentation. And while today’s credit standards have loosened over the past two years, they are still much higher than they were at the time of the collapse. So while homebuyers can once again obtain a loan with a low down payment, they will do so by being held to a higher standard.

What does this mean for you?

If you’ve been on the sidelines, wishing you could get into the homeownership game, but haven’t had the downpayment to do so. It’s time to put on your helmet! With this new 3% down payment option, you should be able to take a big step towards fulfilling your dream of owning your own home. For those who already own their home, it might give you the flexibility to move up into home that might better suit your current living situation. If you have any questions, as always, don’t hesitate to contact me, Troy Stavros with Gables & Gates, REALTORS. I’m here to serve you!

Home Price Trends in Farragut, Knoxville & Beyond

I recently wrote an article that talked about why homeownership far outweighs renting when it comes to building net worth and also posted another article about why a billionaire says buying a home to live it is the single best investment. One of the most important factors when seeing if owning a home is a good investment, is to look at the quality of that investment over time. We can do that by looking at the home price trends in Farragut, Knoxville, and beyond. We all know from looking at the stock market that investments fluctuate. Some years they go up, other times they go down, but most experts say it’s important to buy and hold an investment to allow it to really be fruitful. That’s what we typically do with owner occupied real estate. We buy it to live in for years to come. Let’s see how our investment would have done if we bought over the last few years.

I recently wrote an article that talked about why homeownership far outweighs renting when it comes to building net worth and also posted another article about why a billionaire says buying a home to live it is the single best investment. One of the most important factors when seeing if owning a home is a good investment, is to look at the quality of that investment over time. We can do that by looking at the home price trends in Farragut, Knoxville, and beyond. We all know from looking at the stock market that investments fluctuate. Some years they go up, other times they go down, but most experts say it’s important to buy and hold an investment to allow it to really be fruitful. That’s what we typically do with owner occupied real estate. We buy it to live in for years to come. Let’s see how our investment would have done if we bought over the last few years.

Farragut TN Home Price Trends

- From 2013 to 2014 median home price went up by 15.72%

- From 2012 to 2013 median home prices went down by -4.07%

- From 2011 to 2012 median home prices went down by -2.64%

- From 2010 to 2011 median home prices went up by 2.71%

- From 2009 to 2010 median home prices went up by 2.52%

- From 2008 to 2009 median home prices went down by -12.24%

- From 2007 to 2008 median home prices went up by 10.55%

- From 2006 to 2007 median home prices went down by -3.42%

- From 2005 to 2006 median home prices went up by 6.26%

- Today’s median sale price in Farragut is $315,750 compared to $265,000 in 2006.

So, these numbers show us that over the last 10 years, even going through the real estate downturn, the average home in Farragut saw a price appreciation of 15.39%.

Knoxville TN Home Price Trends

- From 2013 to 2014 median home price went up by 2.66%

- From 2012 to 2013 median home prices went up by 4.72%

- From 2011 to 2012 median home prices went down by -1.36%

- From 2010 to 2011 median home prices stayed flat at 0.00%

- From 2009 to 2010 median home prices went down by -0.07%

- From 2008 to 2009 median home prices went down by -5.41%

- From 2007 to 2008 median home prices went down by -4.52%

- From 2006 to 2007 median home prices went up by 3.74%

- From 2005 to 2006 median home prices went up by 6.80%

- Today’s median sales price in Knoxville is $149,900 compared to $145,000 in 2006.

This shows us that Knoxville as a whole over the last 10 years, even after the housing downturn, the Greater Knoxville area saw a price appreciation of 6.56%.

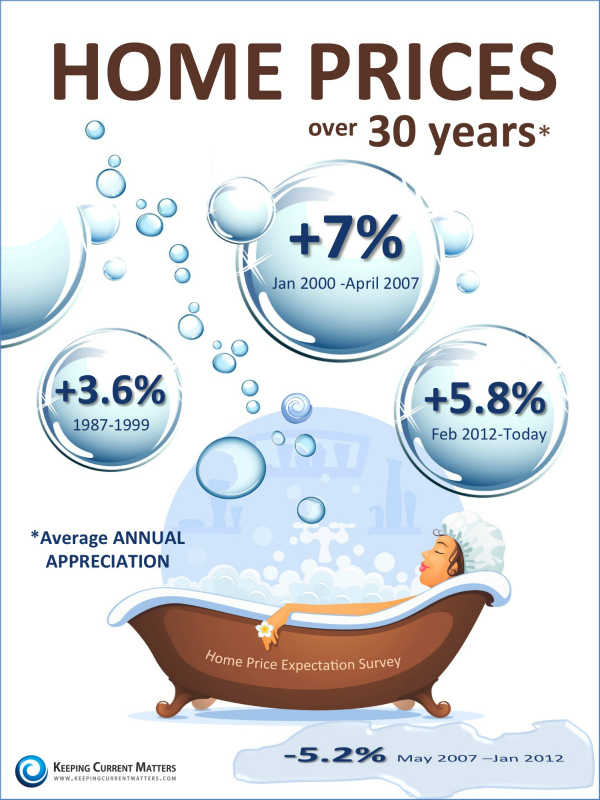

National Home Price Trends

The infographic below shows the history of appreciation in the national housing market:

What does this mean for you?

While the numbers above might not look like a home run investment as far as percentage increases go, ask yourself, what other investments can you live in and enjoy with your family? What other investments can you pay down and build equity in? What other investments can you sell after two years and keep all of the profit that you’ve made, tax free! I don’t know of any others. Plus, have you seen what your money earns in the bank lately?

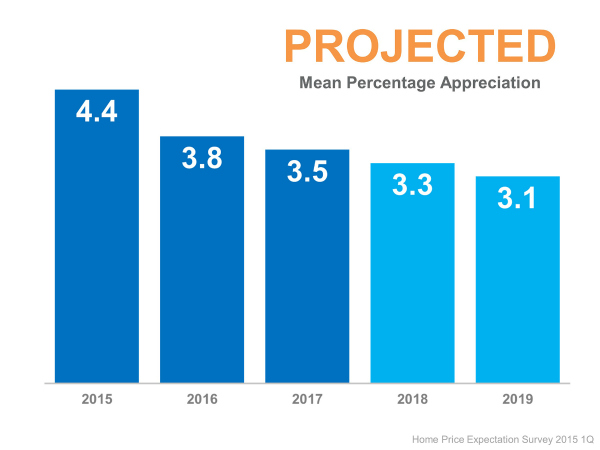

The following graphic shows what experts predict as far as home price trends over the next 5 years:

Keep in mind that all of the numbers above are median averages, and always remember that real estate is local. Local, down to the side of the street you live on sometimes. Your neighborhood might be appreciating significantly more or less when compared to one across town for various reasons. This is why it’s important to find a trusted real estate advisor, who knows the local Farragut real estate or Knoxville real estate markets. If you have questions about the market in your neighborhood, or want to know how much your home could sell for today, feel free to contact me, Troy Stavros with Gables & Gates, REALTORS and I would love to help. I am here to serve you!

Searching Homes for Rent Knoxville TN? Think again!

Are you ready to get out of an apartment and into something larger? Searching homes for rent Knoxville TN? You might want to think twice about that. Here is why. A recent study by the National Association of REALTORS® that studied “income growth, housing costs and changes in the share of renter and owner-occupied households over the past 5 years in metropolitan statistical areas throughout the U.S.,” showed that over the last 5 years, average rent rose 15%, yet the income of the renters only rose 11%. For those currently renting, the difference between rent and income could get you stuck in a place where it becomes impossible for you to save up the funds for a down payment on a home.

Are you ready to get out of an apartment and into something larger? Searching homes for rent Knoxville TN? You might want to think twice about that. Here is why. A recent study by the National Association of REALTORS® that studied “income growth, housing costs and changes in the share of renter and owner-occupied households over the past 5 years in metropolitan statistical areas throughout the U.S.,” showed that over the last 5 years, average rent rose 15%, yet the income of the renters only rose 11%. For those currently renting, the difference between rent and income could get you stuck in a place where it becomes impossible for you to save up the funds for a down payment on a home.

THE BENEFITS OF HOME OWNERSHIP

One of the biggest benefits of homeownership is the ability to protect yourself from rising rents and have a fixed dollar amount for your housing costs for the life of your mortgage. Did you know that there is a good chance that your monthly living expenses will go down if you buy a home? That’s right! Many buyers find that their mortgage payments are less than what they were paying in rent.

The other huge benefit of home ownership is forced savings and building your net worth. The Federal Reserve conducts the “Survey of Consumer Finances” every 3 years where they collect data across all social and economic groups. Here are some of their findings:

- The average American family has a net worth of $81,200.

- 61.4% or $49,856 of that net worth is home equity.

- A homeowner’s net worth is 36X greater than a renters!

- The average renter has a net worth of $5400 while the average homeowner has a net worth of $194,500.

THE REAL DIFFERENCE BETWEEN RENTING AND OWNING

You might be asking yourself why the numbers above are so different. Here is a practical example. A renter, who has rented year after year, is paying their landlord’s mortgage for them. We know that over that last 5 years rent has risen by 15%. So each year the renter is paying more rent to their landlord, yet that renter’s income might not be rising at the same pace as their rent. Therefore over time it effects their net worth negatively. A homeowner on the other hand, has a fixed dollar amount to pay for their housing, because they locked in their interest rate and monthly mortgage payment for up to 30 years when they purchased their home. When they pay their mortgage payment every month, a portion of that payment goes to interest (to pay the bank) and the other portion goes to principal (which pays down the balance of their loan). Whether or not their income increases or not, we know that home values are projected to increase by an average of 3.5% per year for the next 5 years. As the homeowner pays down their balance and the value of their home increases, this builds their home equity, which in turn builds their net worth. It’s no wonder that billionaire investor, John Paulson, recently stated, “I still think, from an individual perspective, the best deal investment you can make is to buy a primary residence that you’re the owner-occupier of.” (you can read that article HERE)

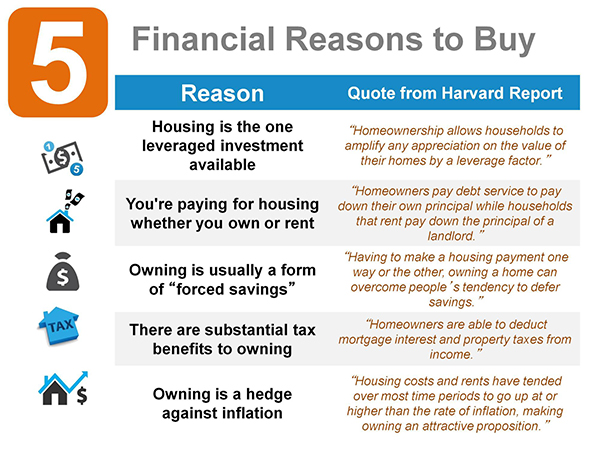

If the example above wasn’t convincing enough, here are 5 financial reasons to buy a home.

I CAN’T QUALIFY FOR A MORTGAGE. ARE YOU SURE?

Another study has found that many renters have actually saved up the amount of money necessary for a down payment on a home, but they don’t think they’ve saved enough or think they can’t qualify for a loan. Unfortunately, this simply isn’t true, even if you’ve had a short sale, foreclosure, or bankruptcy in the past.

According to Freddie Mac: “Depending on their credit history and other factors, many borrowers can expect to make a down payment of about 5-10%. And new 3% down financing options for qualified borrowers could mean a down payment as little as $6000 for a $200,000 home.”

HOW CAN I FIND OUT IF I CAN BUY?

If you are searching homes for rent in Knoxville, it’s time get off the rental roller coaster and stop the cycle of rising housing costs. Many have been caught in this trap. You might be ready and willing to buy a home, but don’t think you are able. Let’s change that! Contact me, Troy Stavros with Gables & Gates, REALTORS today and I will walk you through the EASY process of finding out if you are in a position to buy a home. Take this huge step towards increasing your net worth and more financial freedom. I hope to talk with you soon!

Thinking of Buying a Home Soon? Don’t Run Out Of Luck!

Are you thinking of buying a home in Farragut or Knoxville soon? Don’t let your luck run out! With the 30 year fixed mortgage rates still below 4%, you might be on the fence about buying now or waiting, because you think you still have plenty of time to lock in a low interest rate. However, you might change your mind when you see what the experts predict will happen to rates over the next year.

Are you thinking of buying a home in Farragut or Knoxville soon? Don’t let your luck run out! With the 30 year fixed mortgage rates still below 4%, you might be on the fence about buying now or waiting, because you think you still have plenty of time to lock in a low interest rate. However, you might change your mind when you see what the experts predict will happen to rates over the next year.

Predictions for 2016 (2nd Quarter)

- Fannie Mae Predicts 4.2%

- Freddie Mac Predicts 4.7%

- Mortgage Bankers Association Predicts 4.9%

- National Association of REALTORS® Predicts 5.3%

Let’s take a look at what even a small, .5% increase in the rate could do to the net worth of your family.

Today, on a $250,000 home, with an interest rate of 3.86%, your monthly payment (principal and interest only) would be $1,173.

The Home Price Expectation Survey projects home prices will rise approximately 4.4% in the next year. So in a year, the home above would cost $11,000 more and now be $261,000. If we add on top of that the mortgage rate increase projection of Freddie Mac (about an average of all the projections) at 4.7%, the monthly mortgage payment on the same home rises to $1,354.

That is an increase of $181 per month. And if you think that’s a big chunk of change, let’s multiply it over the course of a 30 year mortgage. Ready? You pay $65,160 more, just because you waited a year to buy.

What does this mean for you?

Well, it’s pretty obvious what it means for you as a buyer. Waiting is going to cost you quite a bit of money. It’s going to shrink your buying power and affordability. That means you will be able to afford more house now, than you will in a year from now (if your income level stays the same).

What does it mean for sellers? Well, what do sellers become after they sell? Buyers! So the same holds true for you. If you are waiting to sell your home because you think it will be worth more in a year, guess what, so will the house you will be eventually buying. Then add the higher interest rate on top of that.

So what this means for you is that there is no better time to buy and sell than right now. If you are interested in talking more about any of the information above or want to discuss buying a home, or selling a home in Farragut or Knoxville, as always, don’t hesitate to contact me, Troy Stavros with Gables & Gates, REALTORS. We’ll find a time that is convenient for you to sit down and discuss your plans and goals and how to best get them accomplished. I look forward to talking with you!

- « Previous Page

- 1

- …

- 84

- 85

- 86

- 87

- 88

- …

- 115

- Next Page »