You’ve found it! Your convenient cabin in the woods that is only minutes from everything you need. Tucked away at the end of a cul-de-sac in Oak Ridge’s Burnham Woods subdivision you’ll find this slice of Tennessee heaven. Literally minutes to shopping, restaurants, and ORNL. This custom built log and stone home features over 3000SF, 5 bedrooms and 3 full baths. Entertain or spread out in 3 separate living areas. Two on the main level feature stone, wood burning fireplaces. The lower level’s extra large rec room is ready for a wood burning stove and and has a separate entrance. Kitchen comes complete with stainless steel appliances. Long covered front porch plus enjoy complete privacy on the covered back porch. 1 car garage. This home was completely remodeled less than 2 years ago.

This listing is no longer available.Females Are Making It a Priority to Invest in Real Estate!

Everyone wants a place to call home; a place that gives them a sense of security. We are currently seeing major interest from females who want to achieve this dream, and the numbers are proving it!

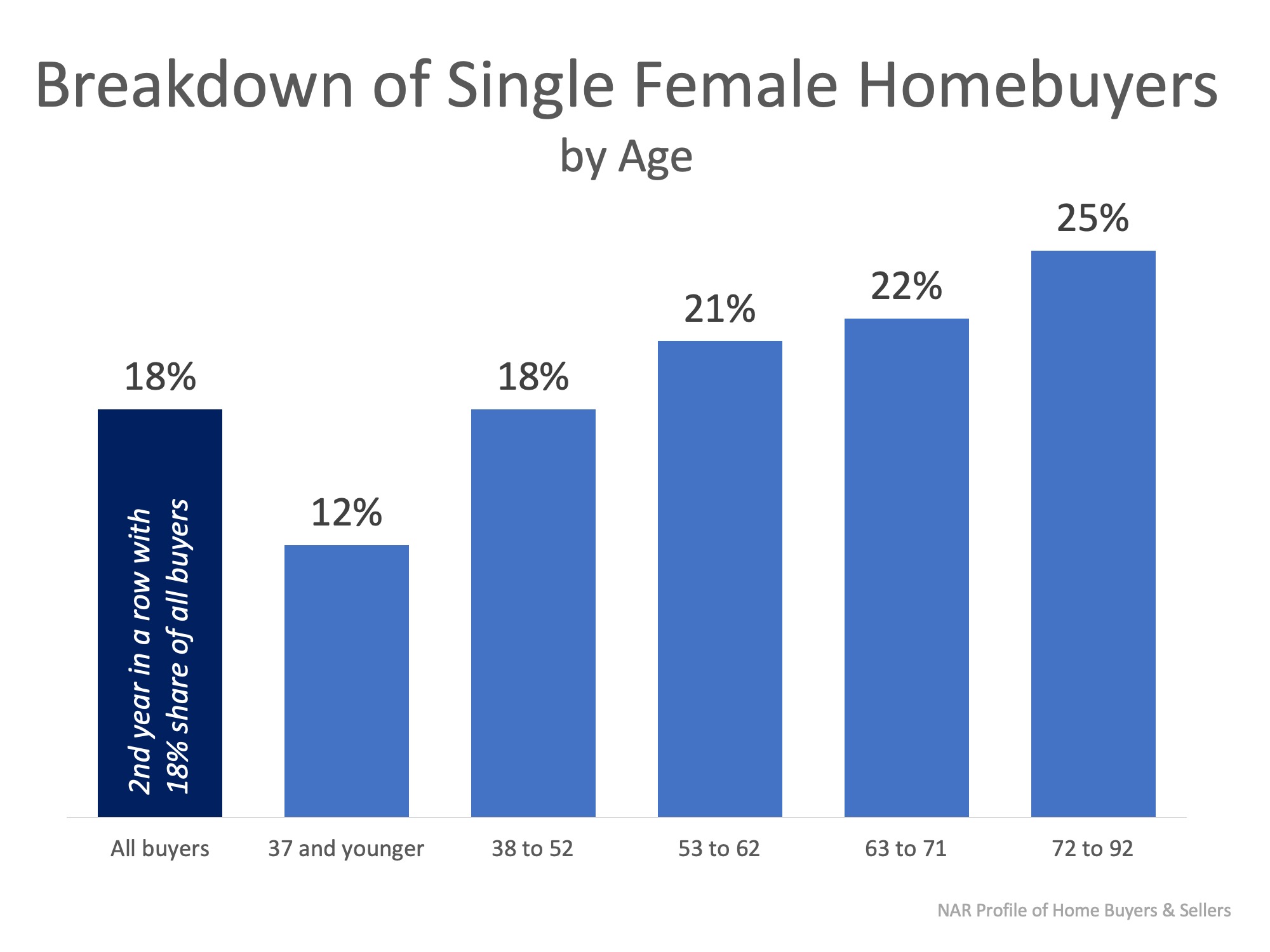

In 2018, for the second year in a row, single female buyers accounted for 18% of all buyers. In 2017, 60% of millennial women listed as the primary borrowers on mortgages were single.

According to the 2018 Home Buyer and Seller Generational Trends Report by the National Association of Realtors, one in five homebuyers in the U.S. were single females (most of them part of the baby boomer generation) as you can see in the graph below:

This does not come as a surprise since 50.8% of the U.S. population is female and 15.6% of them are 65 years and over, according to the Census Bureau.

What are the reasons for this demographic’s booming interest in homeownership?

Bankrate published an article with what they believe to be some of the reasons:

- Divorce rate: Known as the “Gray Divorce,” the divorce rate has doubled for those ages 50 and over and tripled for those ages 65 and over.

- Average life expectancy: For women it’s 81, four years longer than men.

- To build home equity: Women want to build equity through their home. As mentioned by Bankrate, “some are hoping to escape rising rents, some might be downsizing or looking for a new start,” especially those going through a gray divorce.

Are they only downsizing and buying small homes?

Not really; The Institute of Luxury Home Marketing recently stated that:

“The number of female billionaires grew faster globally in 2017 than the number of male billionaires. This redistribution of wealth has seen an impact on luxury real estate both in its purchase and design attributes – and obviously, this is important for realtors to recognize when relating to their clients.”

Bottom Line

Whether you are a millennial who wants to buy a starter home, a billionaire looking for that luxury home you’ve always wanted, or maybe even someone who just went through a gray divorce, let’s get together to help you create your real estate portfolio so that you can start investing your money in real estate today!

Further Proof It’s NOT 2008 All Over Again

Home sales numbers are leveling off, the rate of price appreciation has slowed to more historically normal averages, and inventory is finally increasing. We are headed into a more normal housing market.

However, some are seeing these adjustments as red flags and are suggesting that we are headed back to the same challenges we experienced in 2008. Today, let’s look at one set of statistics that prove the current market is nothing like the one that preceded the housing crash last decade.

The previous bubble was partially caused by unhealthy levels of mortgage debt. New purchasers were putting down the minimum down payment, resulting in them having little if any equity in their homes.

Existing homeowners were using their homes as ATMs by refinancing and swapping their equity for cash. When prices started to fall, many homeowners found themselves in a negative equity situation (where their mortgage was higher than the value of their home) so they walked away which caused prices to fall even further. When this happened, even more homeowners found themselves in negative equity situations which caused them to walk away as well, and so a vicious cycle formed.

Today, the equity situation is totally different. According to a new report from ATTOM Data Solutionsmore than 1-in-4 homes with a mortgage have at least 50% equity. The report explains:

“…nearly 14.5 million U.S. properties were equity rich — where the combined estimated amount of loans secured by the property was 50 percent or less of the property’s estimated market value…The 14.5 million equity rich properties in Q3 2018 represented 25.7 percent of all properties with a mortgage.”

In addition, according to the U.S. Census Bureau, 30.3% of homes in the country have no mortgageon them.

Almost 50% of all homes have at least 50% equity.

If we take both numbers, the 30.3% of all homes without a mortgage and the 17.9% with at least 50% equity (25.7% of the 69.3% of homes with a mortgage), we realize that 48.2% of all homes in the country have at least 50% equity.

Bottom Line

Unlike 2008, almost half of the homeowners in the country are sitting on massive amounts of home equity. They will not be walking away from their homes if the housing market begins to soften.

Buyers: Don’t Be Surprised by Closing Costs!

Many homebuyers think that saving for their down payment is enough to buy the house of their dreams, but what about the closing costs that are required to obtain a mortgage?

By law, a homebuyer will receive a loan estimate from their lender 3 days after submitting their loan application and they should receive a closing disclosure 3 days before the scheduled closing on their home. The closing disclosure includes final details about the loan and the closing costs.

But what are closing costs anyway?

According to Trulia:

“Closing costs are lender and third-party fees paid at the closing of a real estate transaction, and they can be financed as part of the deal or be paid upfront. They range from 2% to 5% of the purchase price of a home. (For those who buy a $150,000 home, for example, that would amount to between $3,000 and $7,500 in closing fees.)”

Keep in mind that if you are in the market for a home above this price range, your costs could be significantly greater. As mentioned before,

Closing costs are typically between 2% and 5% of your purchase price.

Trulia continues to give great advice, saying that:

“…understanding and educating yourself about these costs before settlement day arrives might help you avoid any headaches at the end of the deal.”

Bottom Line

Speak with your lender and agent early and often to determine how much you’ll be responsible for at closing. Finding out that you’ll need to come up with thousands of dollars right before closing is not a surprise anyone is ever looking forward to.

Wage Increases Make Home Buying More Affordable

Everyone knows that housing affordability has been negatively impacted by rising prices and increasing mortgage rates, but there is another piece to the affordability equation – wages.

How much a family earns obviously impacts how easy or difficult it is for them to afford to own a home. Because of an improving economy, wages are finally beginning to increase – and that dramatically affects home affordability.

According to the National Association of Realtors’ (NAR) September 2018 Housing Affordability Index,wages have increased in every region of the country:

After applying current salaries, home prices, and mortgage rates to their Home Affordability Index equation, the index, though still lower than this time last year (160.1 to 146.7), increased over the last month (141.2 to 146.7). For the complete methodology used by NAR, click here.

The percentage of income needed to own a home has also decreased each of the last three months. It currently sits at 17% which is substantially lower than historic numbers.

Bottom Line

If you are a first-time buyer or a move-up buyer who believes that purchasing a home is not within your budget, let’s get together to determine if that is still true.

Home Sellers in Q3 Netted $61K at Resale

According to a recent report by ATTOM Data Solutions, home sellers who sold their homes in the third quarter of 2018 benefited from rising home prices and netted an average of $61,232.

This is the highest average price gain since the second quarter of 2007 and represents a 32% return on the original purchase prices.

After the Great Recession, many homeowners were left in negative equity situations but home price appreciation in the recovery period since then has given homeowners something to smile about.

The results from ATTOM fall right in line with data from the latest edition of the National Association of Realtors’ (NAR) Profile of Home Buyers and Sellers. Below is a chart that was created using NAR’s data to show the percentage of equity that homeowners earned at the time of sale based on when they purchased their homes.

Even though those who purchased at the peak of the market netted less than those who bought before and after the peak, the good news is that there was a double-digit profit to be had! Many homeowners believe that they are still underwater which has led many of them to not even consider selling their houses.

Bottom Line

If you are curious about how much equity you’d earn if you sold your home, let’s get together to perform an equity review and determine the demand for your home in today’s market!

- « Previous Page

- 1

- …

- 57

- 58

- 59

- 60

- 61

- …

- 115

- Next Page »